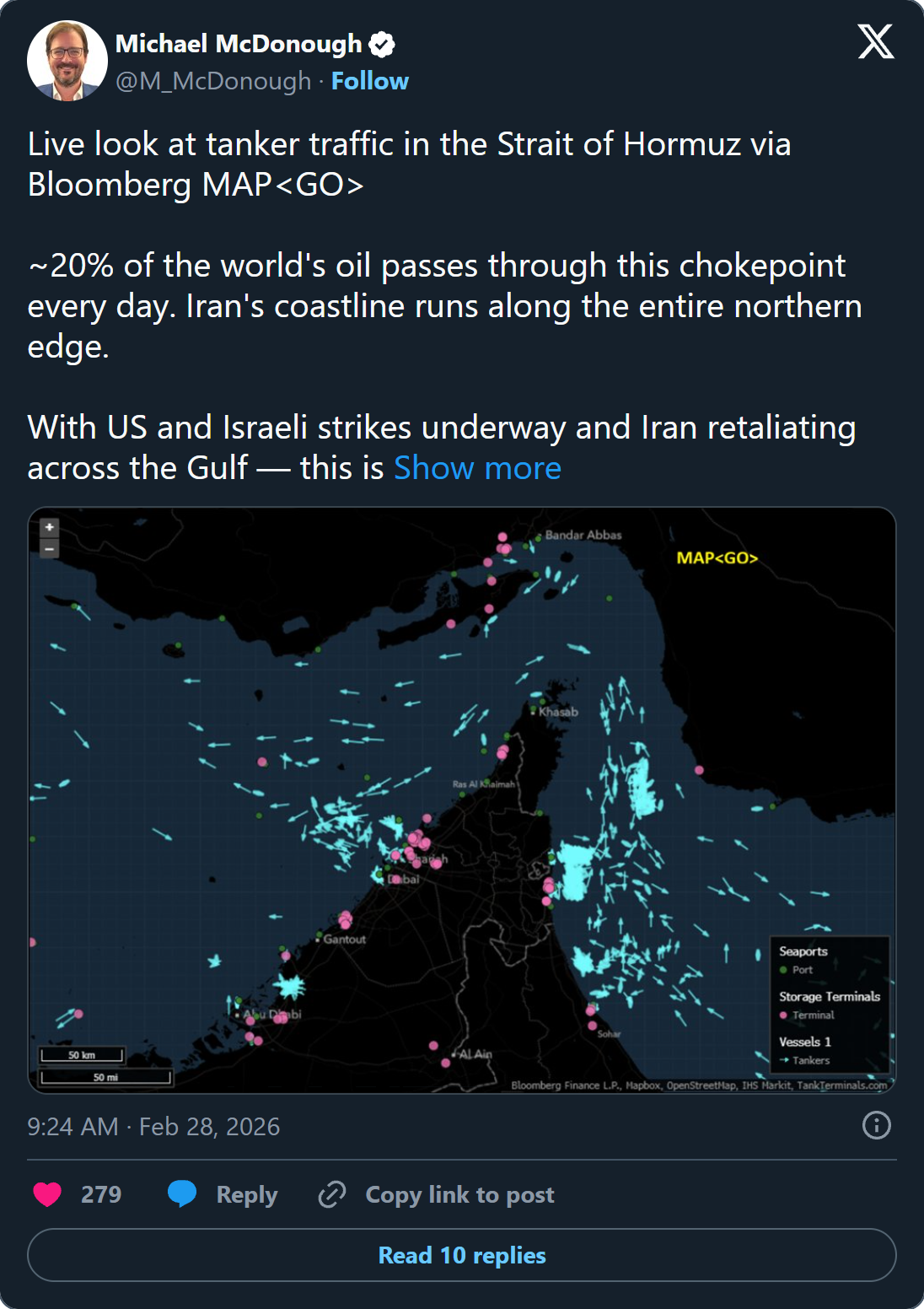

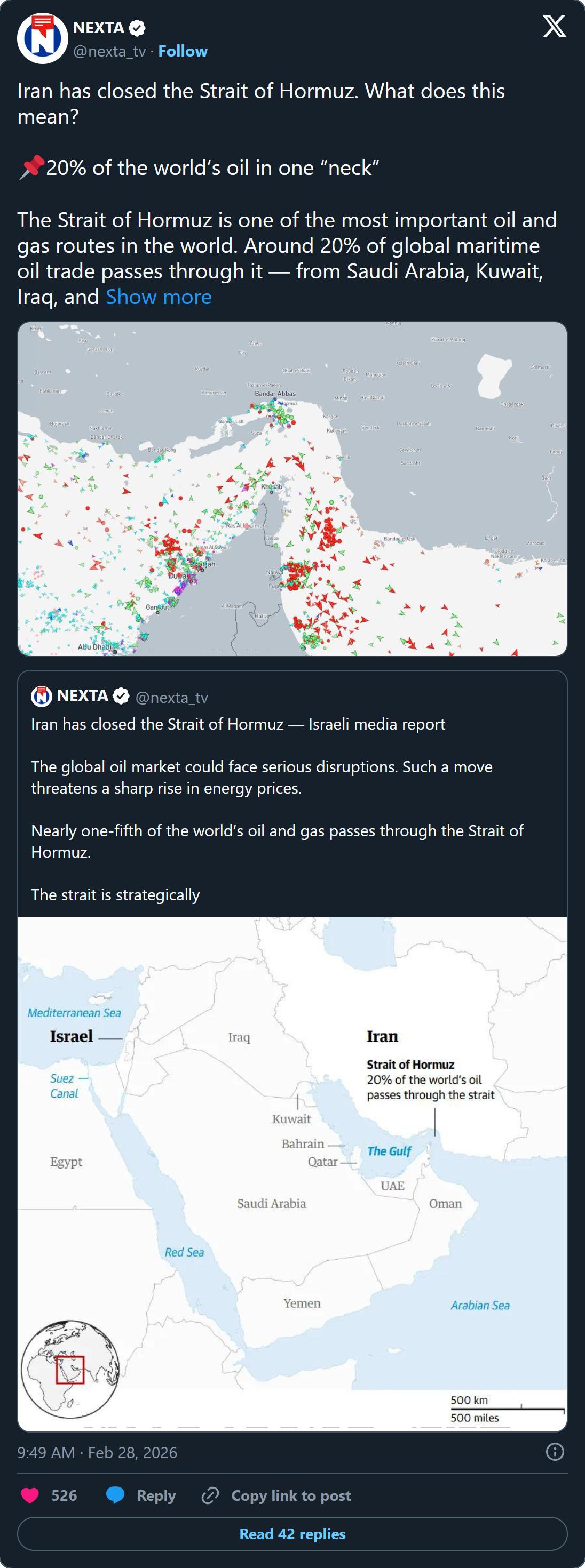

The Strait of Hormuz — a 21-mile-wide chokepoint between Iran and Oman — has functioned for decades as the jugular vein of global energy markets. Approximately 20% of the world's traded oil and 20% of global LNG transits this narrow passage daily, making it the single most consequential maritime corridor on earth. In late February and early March 2026, it became the epicenter of the most dangerous geopolitical crisis since the Cold War.

What began as a targeted U.S.-Israeli strike campaign against Iranian nuclear and military infrastructure rapidly escalated into a multi-theater conflict, with Iran closing the strait, mining shipping lanes, attacking Gulf energy infrastructure across nine nations, and drawing in naval forces from Europe, the United States, and China. The crisis has disrupted an estimated 15–20% of global oil supply — a magnitude exceeding any single disruption in post-war history — and triggered emergency responses from the IEA, the White House, and commodity markets from Tokyo to Rotterdam.

This analysis examines the full strategic picture: the military operations, the energy market rupture, the diplomatic fragmentation, and the scenarios that will determine whether the world faces a prolonged supply shock or a managed de-escalation.

Timeline of the Crisis: From Strikes to Strait Closure

Operation Midnight Hammer and Its Aftermath (Late February 2026)

The chain of events that produced the Hormuz crisis traces back to a prior Israeli unilateral operation — "Operation Midnight Hammer" — that targeted Iranian nuclear enrichment infrastructure in late 2025. That operation, while tactically successful in degrading centrifuge capacity at Fordow and Natanz, triggered a security lockdown inside the Iranian Revolutionary Guard Corps (IRGC) and prompted Tehran to accelerate dispersal of its leadership and command-and-control nodes.

U.S. and Israeli intelligence services spent the subsequent months mapping the new command structure. According to CSIS analyst Emily Harding, operatives had confirmed locations for senior leadership 10–12 hours before the strikes — a remarkable intelligence achievement given the post-Midnight Hammer security purges Iran had undertaken.

The Joint Strike Campaign (Late February – March 1, 2026)

Over approximately 72 hours straddling the final days of February 2026, U.S. and Israeli forces conducted a coordinated strike campaign targeting roughly 2,000 sites across Iranian territory. The target set encompassed missile compounds, command-and-control infrastructure, air defense nodes, ballistic missile production facilities, naval assets, and — critically — regime leadership.

The strike package employed both stealth platforms (F-35s, F-22s) and conventional aircraft (F-16s), achieving a degree of air dominance over Iranian airspace that CSIS defense analyst Seth Jones described as having been accomplished "remarkably quickly" — a feat Russia had failed to achieve over Ukraine in four years of intensive operations. Four U.S. service members were killed; three fighter jets were lost in a friendly-fire incident over Kuwait.

The strategic centerpiece of the campaign was the decapitation of Iranian leadership. Supreme Leader Ayatollah Ali Khamenei and approximately 40 senior officials were killed in the strikes. Iran subsequently established a transitional council to manage succession, though the identity and legitimacy of a successor remained unclear amid ongoing security threats and intense internal power struggles.

Iranian Retaliation: Nine Nations, One Strait (March 1–3, 2026)

Iran's retaliation was immediate, broad, and deliberately aimed at maximizing regional economic disruption rather than U.S. military targets alone. Tehran launched hundreds of drone and missile strikes — including Shahed-type loitering munitions, ballistic missiles, and cruise missiles — against targets in Israel, Bahrain, Kuwait, Saudi Arabia, the UAE, Qatar, Jordan, Iraq, and Oman.

Key infrastructure impacts included:

- Ras Tanura refinery (Saudi Arabia): Saudi Arabia's largest oil refinery, with a processing capacity of 550,000 barrels per day, was forced to halt operations following strike damage.

- Qatar LNG terminal: Production was suspended at facilities handling approximately 10 billion cubic feet per day — roughly 20% of global LNG demand.

- Dubai International Airport: Terminal infrastructure was damaged; airports in Abu Dhabi, Bahrain, and Kuwait were also struck, with airlines suspending thousands of flights and tens of thousands of passengers stranded.

- Oman oil storage: An Iranian drone strike hit Oman's largest oil storage facility, further constraining regional logistics.

On March 1, a ballistic missile attack near Jerusalem killed nine Israelis and injured dozens more. Lebanese Hezbollah — significantly degraded by Israeli operations in 2024 — signaled limited willingness to open a second front, but the Houthis in Yemen retained the capacity to resume Red Sea shipping attacks, adding a second major chokepoint to the threat matrix.

Strait Closure and Mining (March 2–13, 2026)

The most consequential Iranian action was the effective closure of the Strait of Hormuz. Iranian naval forces, operating under IRGC command, deployed mines across shipping lanes within the strait and coordinated small-boat harassment operations against tankers attempting transit. By March 12, a cargo ship had been hit by a projectile in the strait. The Federal Maritime Commission issued warnings about Hormuz surcharges. Shipping analytics firm Windward recorded just 35 Hormuz crossings over four days — a collapse from the normal rate of 20–21 vessels per day that ordinarily carry 17–21 million barrels of oil.

Iran's posture hardened further when U.S. forces struck Kharg Island on March 13 — Iran's primary crude oil export terminal handling approximately 90% of Iranian petroleum exports. Tehran responded by warning that "Gulf energy assets could burn" if Iranian oil infrastructure continued to be targeted, and explicitly threatened that oil prices could reach $200 per barrel.

Military Dimensions

U.S. Naval Posture: "Operation Epic Fury"

The United States deployed significant naval assets to the region under what reporting has identified as "Operation Epic Fury." The operational picture includes:

- Carrier Strike Group presence: Multiple CSGs positioned in the Arabian Sea and Red Sea approaches, providing F/A-18 strike packages and Aegis ballistic missile defense coverage.

- Submarine operations: In a historic first since World War II, a U.S. Navy submarine sank an Iranian frigate using a Mk-48 torpedo in the Indian Ocean, demonstrating willingness to engage Iranian naval assets at range and below the surface.

- Strategic Petroleum Reserve activation: The Trump administration tapped the SPR in response to Iranian shipping attacks, providing a tactical market signal while preparing for extended disruption.

Two surviving Iranian warships sought refuge in Indian and Sri Lankan ports following the submarine strike, creating diplomatic complications for New Delhi — which hosted the vessels while simultaneously maintaining strategic partnerships with Washington.

European Naval Coalition

France deployed the Charles de Gaulle carrier strike group to the Mediterranean, while Italy coordinated with Spain, France, and the Netherlands to position naval assets protecting Cyprus and Europe's southeastern maritime approaches. The European deployment reflects the continent's acute vulnerability to both energy disruption and Iranian retaliation against Mediterranean infrastructure.

Iran's Asymmetric Naval Doctrine

Iran has never planned to win a conventional naval engagement with the United States. Its doctrine is designed to raise the cost of strait transit to unacceptable levels through layered asymmetric pressure:

- Anti-ship ballistic missiles (ASBMs): Iran's Khalij Fars and Hormuz-series missiles are specifically designed to engage large surface vessels, including carriers, at ranges exceeding 300 km.

- Fast-attack craft swarms: IRGC Navy small-boat tactics are optimized for saturation attacks in confined waters where U.S. Aegis systems face detection and tracking challenges.

- Mines: Naval mines represent Iran's most cost-effective denial tool. The strait's relatively shallow depth (70–100 meters in the shipping lanes) makes mine-laying and mine-sweeping both tractable and time-consuming. Clearing a mined strait requires specialized assets — MCMVs (Mine Countermeasure Vessels) — and weeks of careful operations.

- Coastal missile batteries: Land-based anti-ship batteries on the Iranian coastline provide overlapping coverage of the entire strait width.

Munitions Depletion Risk

CSIS analysts flagged a systemic concern with significant strategic implications: U.S. precision munitions stockpiles were already depleted by prior operations before the Iran campaign began. The Tomahawk inventory, JASSM supply, and interceptor stocks have all been drawn down by Ukraine resupply and prior Middle East operations. Sustaining the current operational tempo for weeks carries real risk of constraining U.S. response options in a simultaneous contingency — most critically, a Taiwan Strait crisis.

Energy Market Rupture

Scale of the Disruption

The Strait of Hormuz carries approximately 17–21 million barrels of crude oil and petroleum products per day — roughly one-fifth of global oil consumption. Add LNG exports from Qatar (the world's largest LNG exporter, with most of its output transiting the strait), and the chokepoint represents an unparalleled concentration of energy flow.

The 2026 crisis has produced a supply disruption that market analysts are calling the largest in recorded history. The combined impact includes:

| Disruption Component | Volume Lost |

|---|---|

| Ras Tanura refinery halted | 550,000 bbl/day |

| Qatar LNG terminal suspended | ~20% global LNG demand |

| TotalEnergies production halted | ~15% company-wide; ~10% global supply |

| Saudi output reduction (20% cut) | ~2 million bbl/day equivalent |

| Hormuz transit collapse | 17–21 million bbl/day at risk |

| Oman storage disruption | Regional logistics compromised |

The critical chokepoint factor is Iran's 3 million barrels per day of spare global capacity — the buffer the world normally relies upon to absorb supply shocks. That spare capacity sits on the Iranian side of the strait or requires strait transit. It cannot be rerouted.

Price Response

Oil markets have moved sharply, though the initial response was more muted than the physical disruption might suggest — a pattern consistent with market skepticism about escalation duration:

- Brent crude: $103.10/barrel (+2.67% on March 13-14) — up from approximately $75–80 pre-crisis

- WTI crude: $98.71/barrel (+3.11%)

- Goldman Sachs forecast: Raised Brent target above $100 for March; other institutions projecting $150 in an extended disruption scenario

- Iran's threat: Official statements warning of $200/barrel if Iranian oil infrastructure continues to be targeted

- Natural gas: Spiked approximately 50% same-day as Qatar LNG suspension

- Gasoline: $3.041/gallon (U.S. average), with accelerating upward pressure

- Bank of America advisory: Warning clients to sell oil above $100, citing historical government intervention at that threshold

CSIS energy analyst Clay Seigle characterized the market's relatively modest initial price response as reflecting "a discrepancy between actual risk and market expectations" — with triple-digit oil as the baseline scenario if disruptions persist, and $150–200 within reach if the strait remains closed for weeks.

IEA Emergency Response

The International Energy Agency activated its emergency coordination mechanism, launching what has been described as a record 400-million-barrel emergency oil release from member state strategic reserves. The United States, in parallel, tapped the Strategic Petroleum Reserve — echoing the 60-million-barrel release coordinated with the IEA during the 2022 Russia-Ukraine supply shock, but at larger scale.

The emergency release is designed to buy time — not replace Hormuz. At current global consumption of roughly 102 million barrels per day, a 400-million-barrel reserve release provides approximately four days of full offset, or several weeks of partial offset against the disruption. It suppresses panic buying and price spikes but cannot substitute for restored physical flows.

Downstream Industrial Impact

China's exposure is acute: Beijing sources approximately 45% of its energy imports from the Middle East Gulf. Sinopec, China's largest refiner, has already slashed refinery run rates by 11–13%. The ripple effects extend downstream to petrochemical production, plastics, fertilizers, and the entire hydrocarbon-dependent industrial base that underpins Chinese manufacturing.

Saudi Arabia — simultaneously a victim of Iranian strikes and the world's swing producer — has sought to reroute some exports. Riyadh offered 2 million barrels for sale via Red Sea routing on March 13, attempting to bypass the Hormuz chokepoint via the East-West Pipeline to Yanbu. However, the East-West pipeline's capacity (approximately 5 million bbl/day) cannot absorb the full volume that normally transits Hormuz from Gulf producers.

Iraq continues pumping approximately 1.4 million barrels per day, but export route options are constrained. Iraqi exports via the Turkish pipeline (Kirkuk-Ceyhan) remain operational but are below full capacity.

Diplomatic Landscape

Gulf State Fragmentation

The Gulf Cooperation Council's response reflects deep strategic ambivalence. Saudi Arabia and the UAE publicly condemned Iranian attacks as "blatant aggression" and "flagrant violations of national sovereignty" — their own territory and infrastructure having been struck. Yet GCC states have shown mixed willingness to formally align with U.S. military operations, calculating that explicit co-belligerence invites further Iranian targeting.

This is the fundamental dilemma of Gulf security architecture: states that host U.S. forces and depend on American deterrence are structurally incentivized to maintain ambiguity rather than overt partnership when conflict becomes kinetic.

China's Strategic Dilemma

Beijing faces perhaps the sharpest strategic dilemma of any external power. China is simultaneously Iran's largest oil customer, a country with 45% energy dependence on Middle Eastern Gulf supplies, and a nation whose global AI infrastructure ambitions are increasingly concentrated in Saudi Arabia and the UAE.

China has refrained from condemning Iranian actions while signaling concern about energy market stability. The CSIS compute-dependence analysis noted that U.S. and Gulf AI infrastructure investments have created "asymmetric interdependence" — Beijing needs Gulf energy and U.S. technology simultaneously, constraining its freedom to escalate diplomatic support for Tehran.

Iran's Succession Crisis

The killing of Supreme Leader Khamenei and approximately 40 senior officials has created a succession vacuum with no historical precedent in the Islamic Republic. The transitional council established in the aftermath faces competing power centers: IRGC factions, the clerical establishment in Qom, pragmatic technocrats, and hardline elements determined to continue the confrontation. CSIS assessed that Iran faces "significant flux" with "intense jockeying" among power centers — a condition that simultaneously reduces the chance of a negotiated off-ramp and increases the risk of miscalculation.

Regime collapse is assessed as a low-probability scenario but non-zero, with CSIS noting potential for provincial fragmentation and refugee flows if central authority breaks down. Historical precedent — Iraq 2003, Libya, Afghanistan — suggests that air-only decapitation campaigns rarely produce stable outcomes, and that the absence of a ground force component makes post-conflict stabilization particularly uncertain.

India's Neutral Corridor

India's decision to host two Iranian warships in Indian ports after the submarine strike has created a notable diplomatic complication. New Delhi is navigating competing interests: its energy dependence on Gulf imports, its strategic partnership with the United States, its longstanding non-alignment posture, and its historical ties with Iran. Indian port access for Iranian naval vessels, while technically neutral, provides Iran a logistical foothold outside the contested Persian Gulf theater.

The Compute Dimension: A New Stakes Variable

The 2026 crisis has revealed a strategic dimension that prior Hormuz crisis analyses did not adequately account for: Gulf states have become critical nodes in global AI infrastructure.

Saudi Arabia and the UAE have committed hundreds of billions of dollars to data center development, attracting hyperscaler investments from Microsoft, Google, Amazon, and a constellation of U.S. AI companies. The 2024 Red Sea cable incidents — which disrupted approximately 25% of Asia-Europe internet traffic — demonstrated how regional conflict extends to digital infrastructure with global consequences.

A prolonged Gulf conflict that damages or threatens this data center infrastructure would impose costs far beyond oil prices. It would disrupt AI training runs, cloud computing availability, and the emerging digital economic architecture that the 21st-century global economy increasingly depends upon. As one CSIS analysis framed it: "If compute is the new oil, war in the Gulf significantly raises the stakes."

This factor adds a new constituency for de-escalation — U.S. technology companies with massive capital exposure in the Gulf — and a new dimension of Iranian leverage that has not yet been fully exercised.

Scenario Outlook

Scenario 1: Negotiated De-escalation (4–6 Weeks)

Probability: Low-Moderate (20–30%)

Iran's transitional council reaches an internal consensus favoring a ceasefire, potentially mediated through Oman (Muscat's traditional back-channel role) or Qatar. The U.S. agrees to halt offensive operations in exchange for strait reopening and mine removal. A transitional government in Tehran receives sanctions relief assurances as an incentive.

Conditions required: coherent Iranian leadership capable of making binding commitments; U.S. willingness to accept a non-regime-change outcome; Gulf state pressure on both parties to end infrastructure targeting.

Oil market outcome: Brent retreats to $75–85 range within 60 days of confirmed strait reopening. LNG prices stabilize. IEA reserves partially refilled.

Scenario 2: Prolonged Standoff (3–6 Months)

Probability: Moderate-High (40–50%)

Iranian transitional council remains internally divided. Mines remain in place. The U.S. conducts mine-clearing operations under naval escort, partially restoring transit, but tanker operators and insurers maintain war-risk surcharges. Iranian forces conduct periodic harassment operations against transiting vessels. Oil flows at 60–70% of normal through the strait.

This is the baseline scenario most consistent with current military and diplomatic dynamics. The absence of a coherent Iranian interlocutor makes a swift negotiated settlement structurally difficult.

Oil market outcome: Brent stabilizes in the $100–120 range. Shipping insurance remains elevated. Alternative routing (East-West pipeline, Cape of Good Hope diversions) absorbs a fraction of diverted volume at higher cost.

Scenario 3: Escalation — Houthi Re-engagement and Dual Chokepoint Crisis

Probability: Moderate (25–35%)

The Houthis resume Red Sea shipping attacks, closing Bab al-Mandab to commercial traffic simultaneously with the Hormuz disruption. This creates a dual chokepoint scenario affecting both the Persian Gulf export corridor and the Europe-Asia shipping lane.

The combined impact would remove alternative routing options. Ships unable to use Hormuz could not take the Suez/Red Sea route either, forcing Cape of Good Hope diversions adding 10–14 days and $500,000–$1,000,000 per voyage in additional fuel and time costs.

Oil market outcome: Brent breaks through $130–150. Gasoline prices spike above $5/gallon in the United States. Global recession risk rises materially. IEA releases prove insufficient; emergency rationing discussions in European capitals.

Scenario 4: Iranian Regime Collapse and Power Vacuum

Probability: Low (10–15%)

Internal power struggles within Iran's transitional council produce a breakdown of central authority. Provincial governors, IRGC regional commanders, and clerical factions pursue competing agendas. Central control over naval and missile forces becomes uncertain.

This scenario paradoxically reduces Iranian capacity for coherent military operations but increases the risk of unauthorized or freelance attacks on Gulf infrastructure by rogue IRGC units. It also creates a humanitarian crisis and refugee flow that draws in regional actors.

Oil market outcome: Deeply uncertain — depends entirely on which factions control Kharg Island and naval assets. Could range from a rapid normalization (if moderate technocrats prevail) to continued disruption under decentralized IRGC command.

Strategic Implications for Global Energy Architecture

The 2026 crisis has exposed three structural vulnerabilities that will reshape energy policy for a generation:

1. The Hormuz Dependency Cannot Be Engineered Away

Decades of discussion about reducing Hormuz dependence through alternative pipelines (East-West, Iraq-Turkey, Abu Dhabi's Habshan-Fujairah pipeline) have produced partial solutions. The UAE's Fujairah bypass handles approximately 2 million barrels per day. Saudi Arabia's East-West pipeline handles 5 million. But the strait still carries 17–21 million barrels daily, and no credible alternative routing exists for that volume within any operational timeframe.

2. Spare Capacity Concentration is a Systemic Risk

The world's remaining 3 million barrels per day of spare production capacity sits almost entirely in Saudi Arabia — capacity that requires Hormuz transit for export. This creates a structural scenario where the very buffer designed to absorb supply shocks is inaccessible during a Hormuz closure. The IEA's emergency release mechanism was designed to address this, but its volume is finite and its replenishment requires return to normal market conditions.

3. The Insurance Market as a Chokepoint

War risk insurance for Hormuz transit has become a de facto second chokepoint. When Lloyd's of London and its syndicates price Hormuz transit insurance at levels that make commercial operations uneconomic, vessels stop — regardless of whether the physical channel is open. Insurance market dynamics have proven faster and more binding than diplomatic or military interventions in restraining tanker movements.

Related Social Posts

What The World Is Saying

FAQ: Strait of Hormuz Crisis 2026

Q: How much oil flows through the Strait of Hormuz, and why can't it be rerouted?

The strait handles approximately 17–21 million barrels of crude oil and petroleum products per day — roughly one-fifth of global oil consumption — plus approximately 20% of global LNG trade. Alternative pipelines exist (the UAE's Fujairah bypass at ~2 million bbl/day, Saudi Arabia's East-West pipeline at ~5 million bbl/day) but collectively cannot absorb even a fraction of normal Hormuz volume. There is no viable large-scale alternative route for the majority of Persian Gulf oil exports.

Q: Is the Strait of Hormuz actually closed, or just disrupted?

As of mid-March 2026, the strait is effectively closed to normal commercial traffic. Iran has laid mines in shipping lanes, IRGC fast boats are conducting harassment operations, and at least one cargo vessel has been struck by projectile fire. Shipping companies have declared force majeure, insurance underwriters have suspended normal coverage, and transit volume has collapsed to a fraction of normal — approximately 35 crossings over a four-day period versus the normal 20–21 vessels per day. The legal right of innocent passage remains formally asserted by the U.S. and international community, but practical access requires naval escort and mine-clearance operations.

Q: What is the IEA doing, and will emergency reserves be enough?

The International Energy Agency has coordinated a record 400-million-barrel emergency release from member state strategic reserves. This is the largest coordinated release in IEA history. However, it provides only days to weeks of full offset against the disruption volume, making it a price-stabilization and panic-prevention tool rather than a supply replacement. The United States has separately tapped the Strategic Petroleum Reserve. These actions are buying time for diplomatic resolution and partial supply rerouting — they cannot substitute for restored Hormuz transit.

Q: What happens to oil prices if the strait stays closed for months?

Goldman Sachs has raised its Brent forecast above $100 for March, with multiple institutions projecting $150 in an extended disruption. Iran has threatened prices could reach $200 if its oil infrastructure continues to be targeted. Bank of America has advised clients to sell above $100, citing historical patterns of government intervention at that threshold. The actual price path will depend critically on whether the Houthis re-engage in the Red Sea (which would create a second chokepoint), whether the IEA releases prove sufficient to dampen panic buying, and how quickly U.S. and coalition naval forces can begin mine-clearing operations.

Q: What is the likelihood of diplomatic resolution, and through what channel?

De-escalation probability is constrained by the fundamental problem of Iranian interlocutor coherence: the transitional council established after Khamenei's killing faces intense internal power struggles among IRGC factions, the Qom clerical establishment, and technocratic pragmatists. Oman has historically served as the back-channel between Washington and Tehran; Qatar has also played this role. But effective mediation requires a counterpart capable of making binding commitments — and Iran's succession crisis makes that uncertain. The most likely near-term pathway is a partial operational pause (halt to offensive strikes in exchange for mine-removal commitment) rather than a comprehensive settlement, with full diplomatic resolution potentially taking months to years.

Analysis based on CSIS reporting, oilprice.com market data, Defense News military coverage, and Maritime Professional shipping intelligence as of March 13–14, 2026. The situation remains highly dynamic; readers should consult current reporting for latest developments.

Related Topics

Related Analysis

EU Secondary Sanctions on China: Risks and Consequences

The Board · Feb 21, 2026

Turkey NATO Membership and Potential Russian Alliance

The Board · Feb 21, 2026

Modern World War 3 Scenarios and Systemic Collapse

The Board · Feb 19, 2026

Two Voices: How Iran's State Media Edits Itself Between Languages

The Board · Apr 15, 2026

China's Taiwan Dictionary: Ten Words Instead of Invasion

The Board · Apr 15, 2026

Seven Days in Baghdad: The Kataib Hezbollah Anomaly

The Board · Apr 15, 2026

Trending on The Board

Seven Days in Baghdad: The Kataib Hezbollah Anomaly

Geopolitics · Apr 15, 2026

Two Voices: How Iran's State Media Edits Itself Between Languages

Geopolitics · Apr 15, 2026

China's Taiwan Dictionary: Ten Words Instead of Invasion

Geopolitics · Apr 15, 2026

The Hormuz Math: Why the Strait Can't Be Reopened Fast

Energy · Apr 15, 2026

Future Surveillance and Control by 2035

Technology · Apr 16, 2026

Latest from The Board

Fauci Aide Morens Indicted: NIH FOIA Officer Named Co-Conspirator

Policy & Intelligence · Apr 28, 2026

Crude Oil Price Forecast WTI Brent

Energy · Apr 25, 2026

Netanyahu Prostate Cancer: A Geopolitical Analysis

Geopolitics · Apr 24, 2026

Salesforce's Agentforce Math Has a Fatal Flaw

Markets · Apr 22, 2026

US-Iran Talks: What's at Stake for the US?

Geopolitics · Apr 21, 2026

Copper Price Forecast $15,000 by 2026

Markets · Apr 18, 2026

Strait of Hormuz Blockade: Is Iran Provoking War?

Geopolitics · Apr 18, 2026

US Strikes Iran Consequences Analysis

Geopolitics · Apr 18, 2026